How to find out whether your money lasts — and how to hold it so it does

If you're trying to answer "will my retirement money actually last?", this is how. A guided, screen-by-screen walkthrough of the Retirement Planner on a real plan: enter your life and spending, project your corpus, and stress-test it against ten thousand Monte Carlo market paths. Then set up how the money is actually held — the categories it sits in, the five-bucket withdrawal strategy, and the glide that de-risks it before you retire — and revisit it as life changes to stay on track. Know enough already? Skip ahead and start the free trial. Otherwise, take the tour.

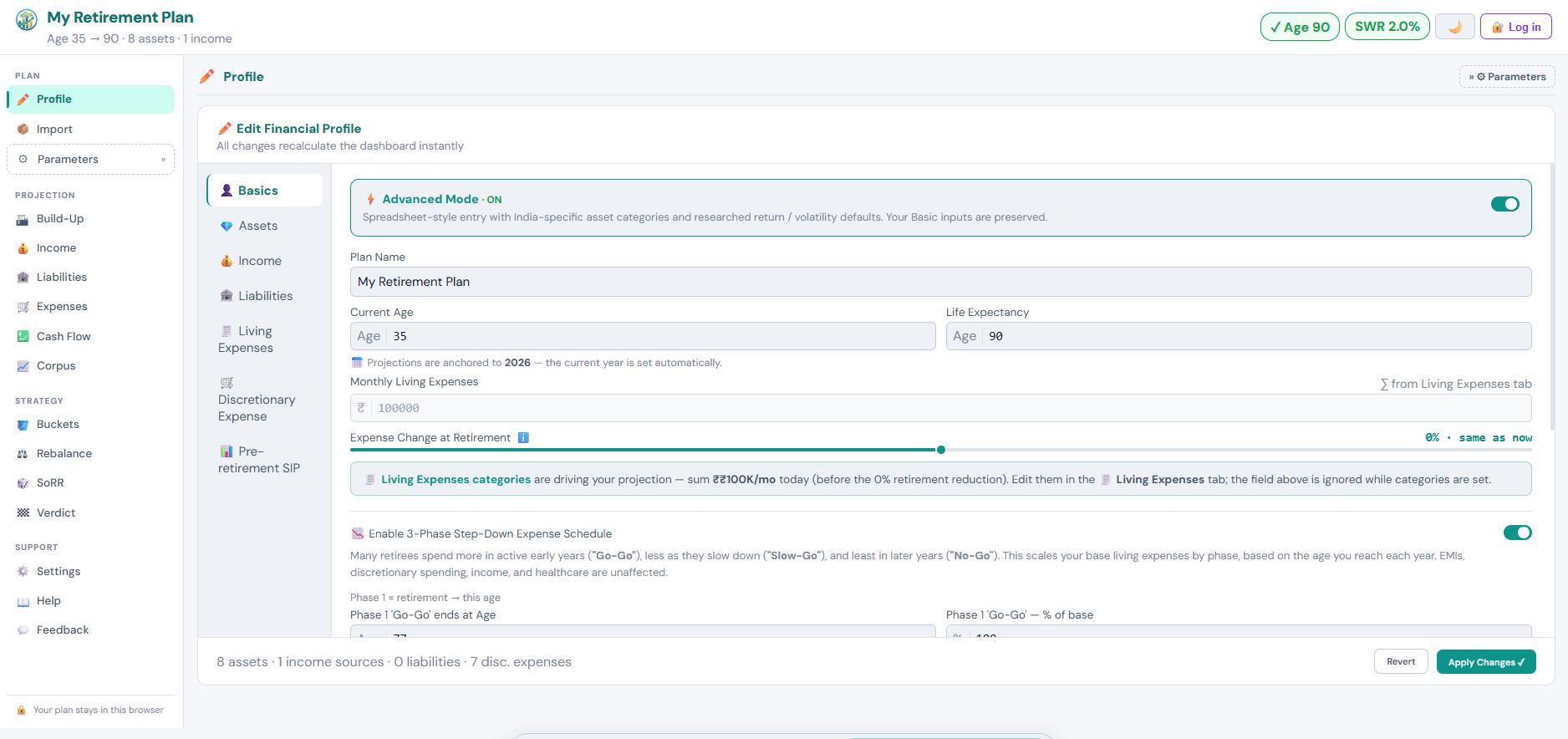

Start here: enter your life, not your portfolio

Fill in your age, how long you plan to live, and what you actually spend. The three-phase step-down lets you model the thing every flat projection gets wrong: people spend more in the active years just after retiring than they do at 85.

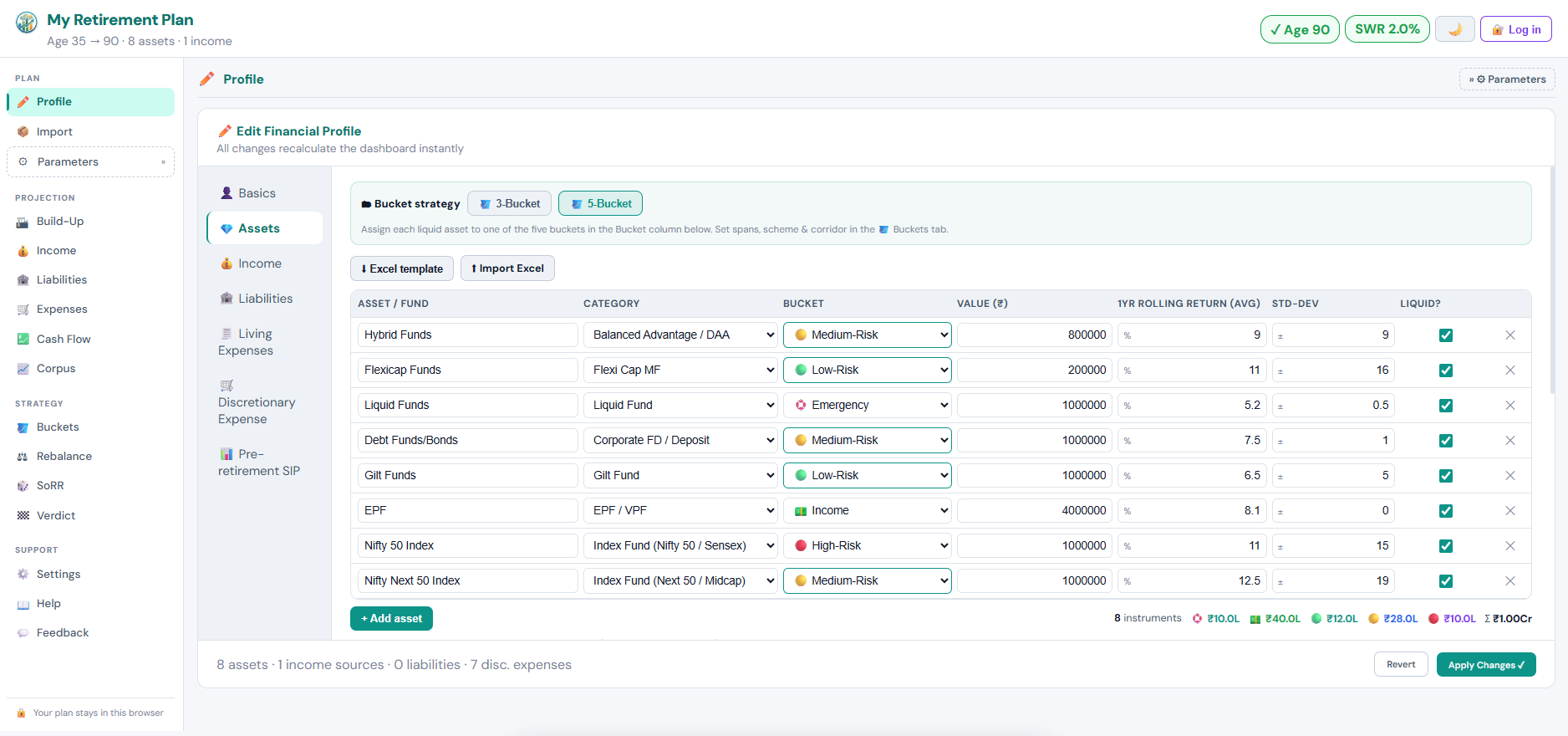

Add your real portfolio, category by category

Enter what you hold as a spreadsheet, using India-specific categories — flexi-cap, gilt, EPF, balanced advantage, index — each carrying a researched return and volatility you can override. Or bring the whole lot in from an Excel template.

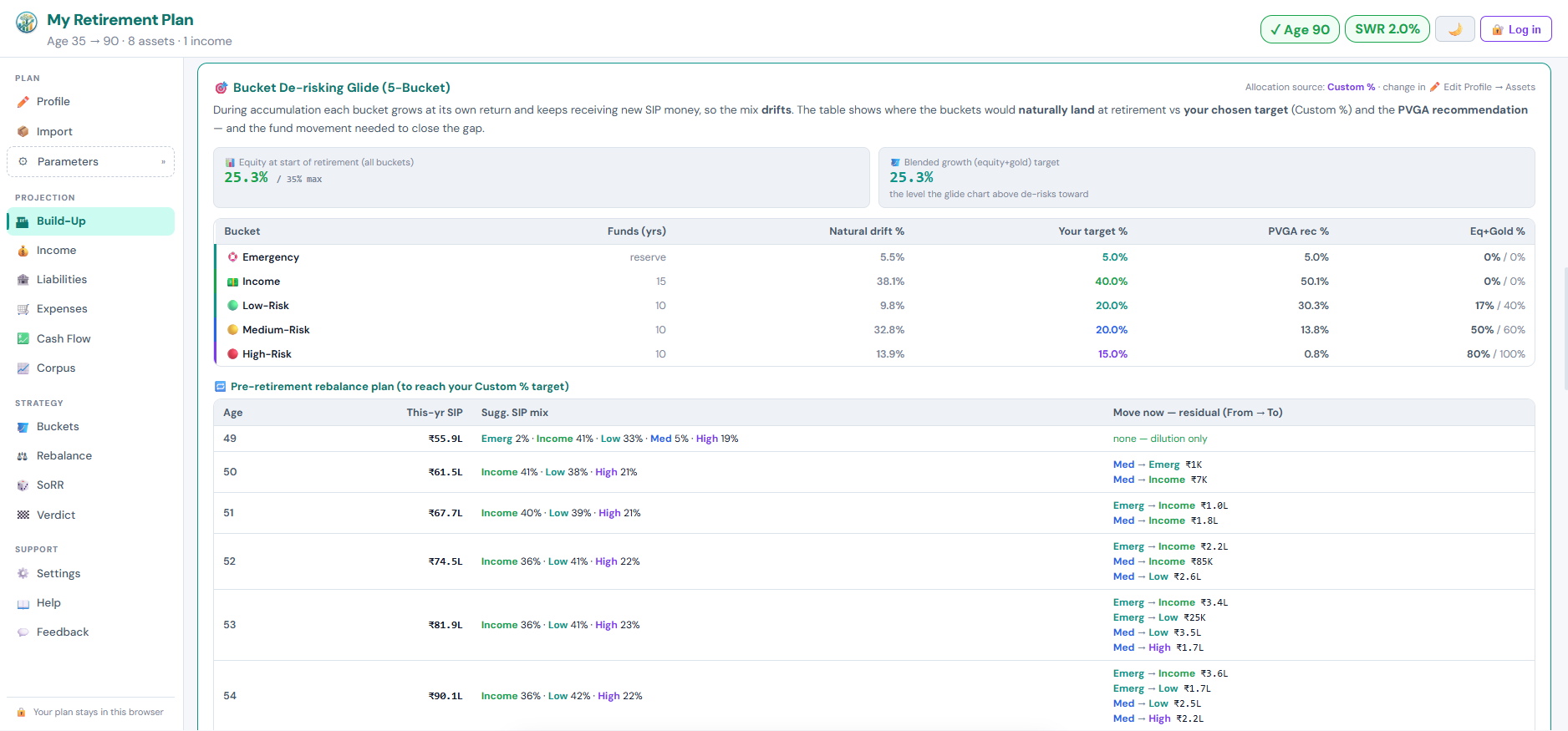

De-risk on a glide, before you retire

While you're still accumulating, your buckets drift — new SIP money and different returns pull the mix around. This shows where they'd naturally land at retirement against your target, and the exact SIP redirection each year that closes the gap.

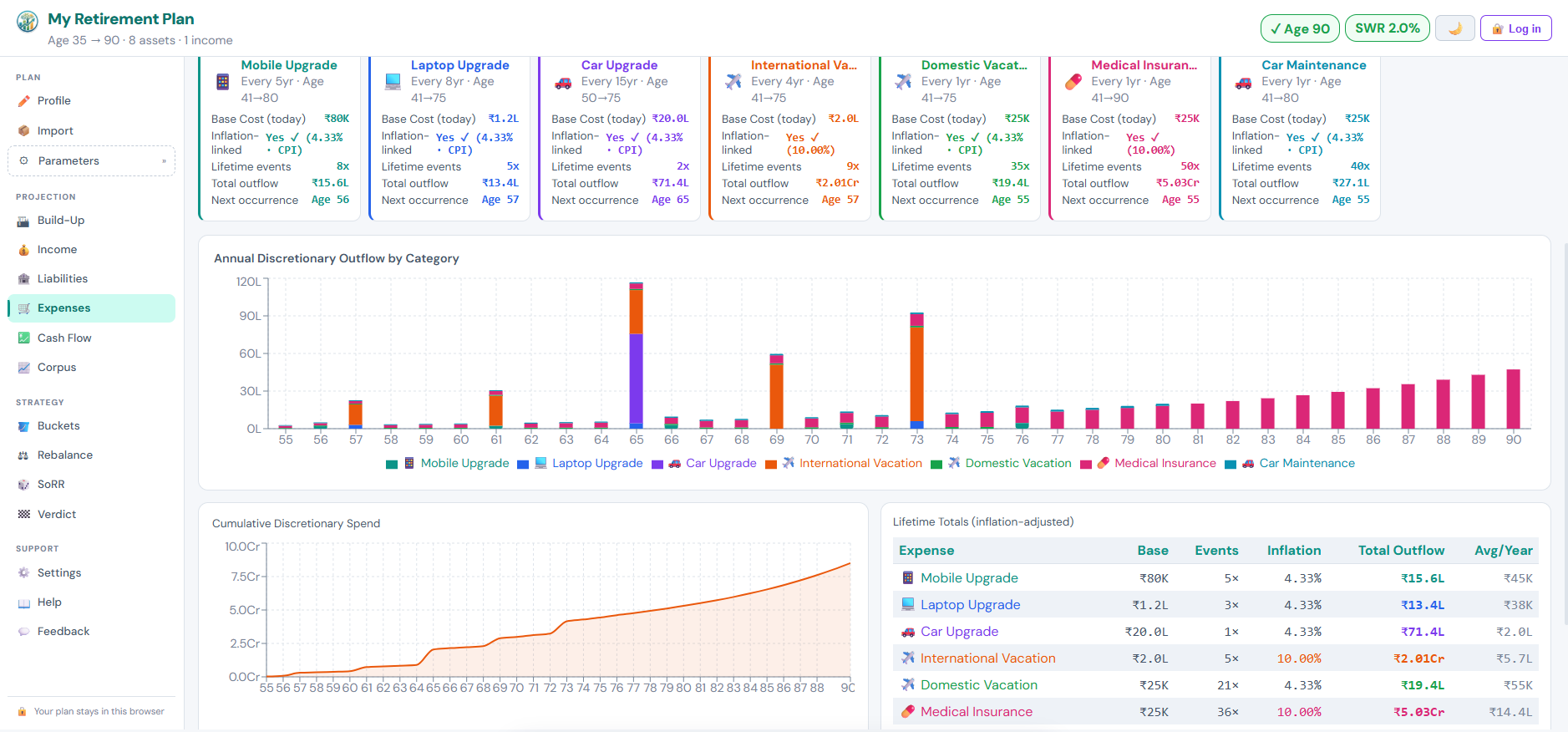

Add the lumpy costs a flat budget forgets

Enter the one-offs: a car every fifteen years, a foreign holiday every four, medical cover every year at its own 10% inflation. Give each its own recurrence and age window — because these are what turn a plan that "just about works" into one that doesn't.

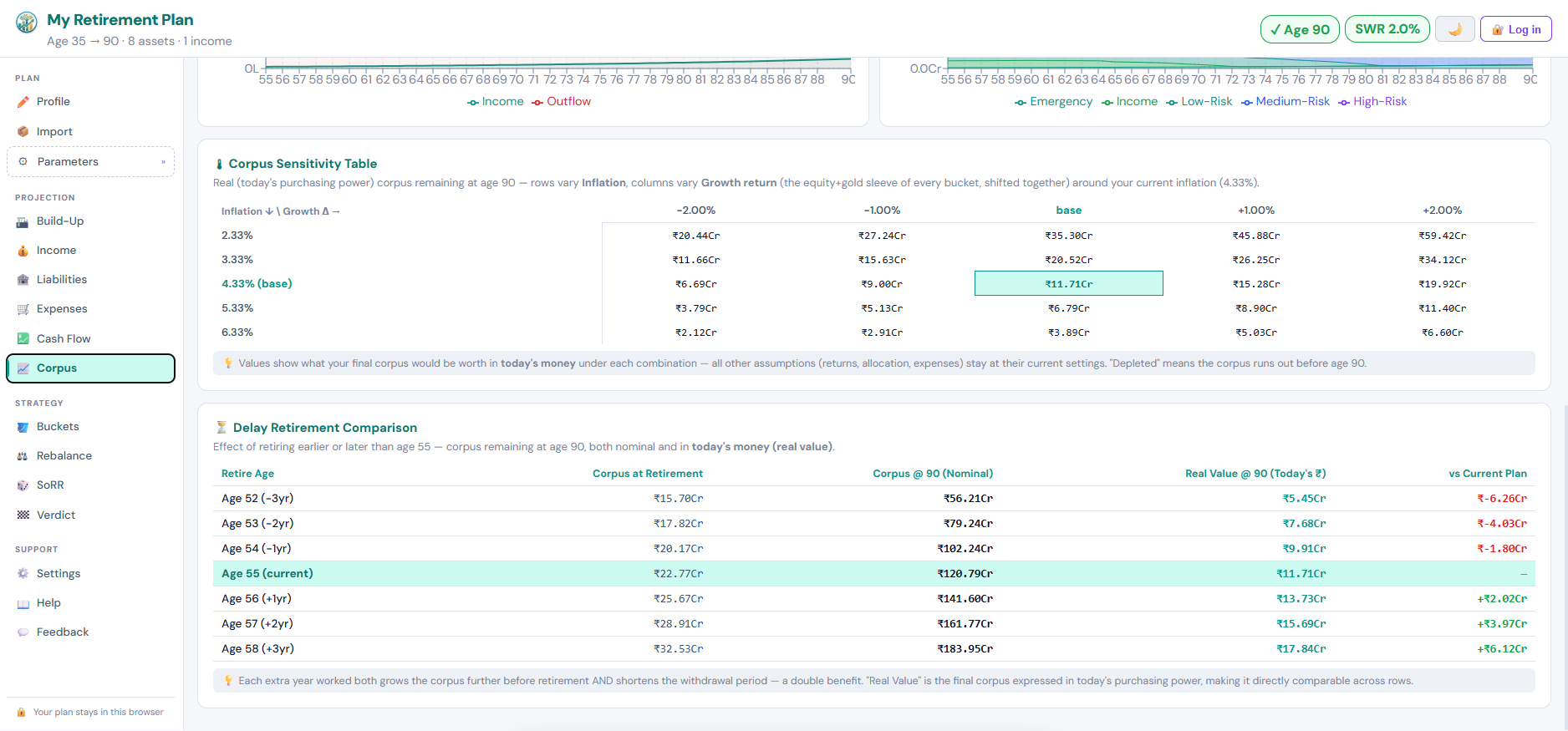

Test what happens if you're wrong on returns

Read your final corpus across a grid of inflation and growth assumptions, in today's money — so you can see how much of the plan rests on being right. Alongside it, check what one more year of work is actually worth.

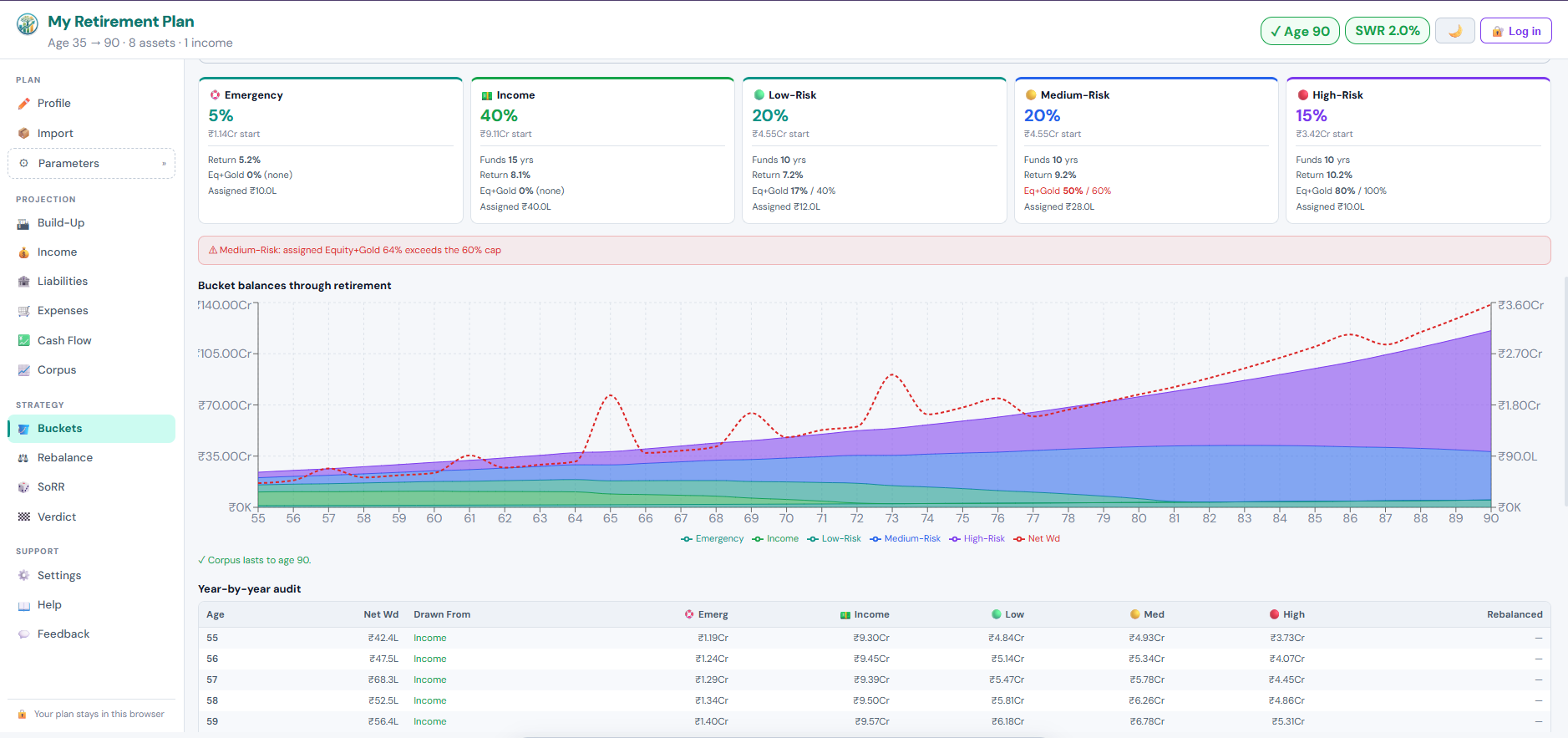

Split the money into five buckets by horizon

Emergency, Income, Low, Medium and High-Risk — time-segmented, so the money you need at 58 was never sitting in equity. The year-by-year audit shows which bucket each withdrawal was actually drawn from.

Set each bucket's corridor and let it rebalance

Every bucket is rebalanced independently to its own equity+gold target whenever it drifts outside the corridor you set. You see the drift, the corridor, and every rebalance event across the whole retirement.

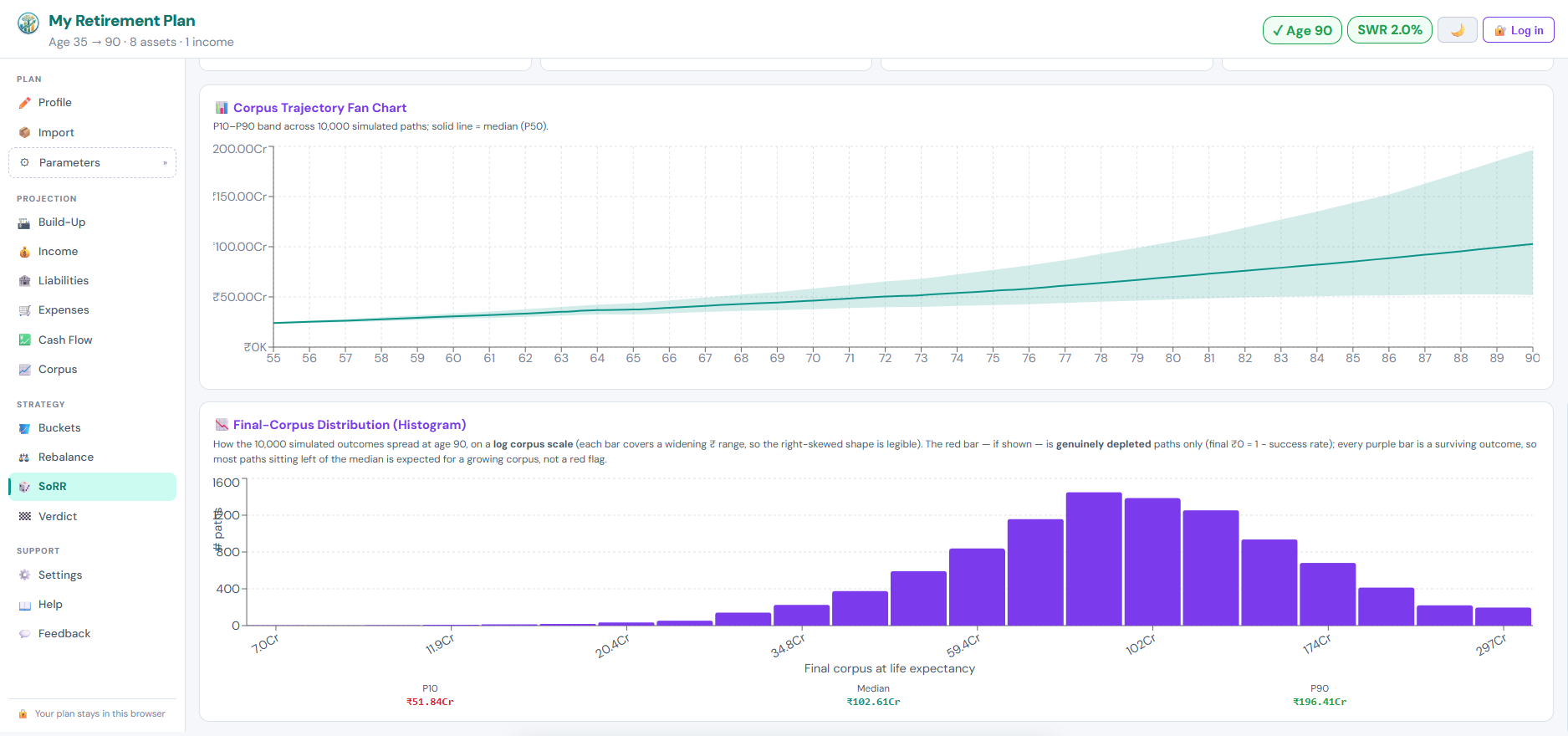

Stress-test it against 10,000 market paths

Averages don't retire you — sequences do. A bad first decade while you're withdrawing can sink a plan whose long-run average was fine. The fan is the P10–P90 band across 10,000 paths; the histogram is where they actually land.

How to use the Retirement Planner, from start to finish

The Retirement Planner exists to answer one question honestly — will my money last, and how should I hold it so it does? — and to keep answering it as life changes. Here's the full order of use. A few of these screens aren't in the tour above; they matter just as much, so they're described here too.

-

1

Enter your life and spending

On Edit Profile, put in your age, how long you plan to live, and what you actually spend. Use the three-phase step-down so the plan reflects spending more in the active early-retirement years than at 85.

-

2

Add your income and liabilities (not shown above)

Record any retirement Income — a pension, rent, an annuity — and any Liabilities still running, like a home loan. The plan nets these against your expenses so the corpus only covers what your other income doesn't.

-

3

Add the lumpy, one-off costs

In Discretionary Expenses, add the big irregular items — a car every fifteen years, a holiday every four, medical cover at its own inflation — each with its own recurrence and age window. These are what quietly break an otherwise-fine plan.

-

4

Read the corpus and the year-by-year cash flow

On Corpus, see your final corpus across a grid of inflation and growth assumptions in today's money, and check what one more year of work is worth. The Cash Flow view (not shown above) lays out every year's inflows, outflows and balance so you can see exactly when money gets tight.

-

5

Get the plain verdict (not shown above)

The Verdict screen gives you the one-line answer — does the plan hold, and with how much room to spare — without making you read a chart to get it. It's the quickest gut-check after any change.

-

6

Stress-test it with Monte Carlo

Open SoRR and run the plan against 10,000 market paths. The P10–P90 fan and the histogram show how a bad first decade could play out — because a plan that survives the average can still fail a bad sequence.

-

7

Enter your real portfolio

Switch to Assets and enter what you hold as a spreadsheet, using India-specific categories with researched returns and volatility you can override — or import it all from an Excel template.

-

8

Choose and tune your withdrawal strategy

The three-bucket strategy is built in. For finer control, Buckets splits the money into the five-bucket time-segmented strategy — Emergency, Income, Low, Medium and High-Risk — and the Bucket Strategy Lab lets you tune the refill rules and see what changes.

-

9

Set each bucket's rebalance corridor

On Rebalance, give each bucket its own equity+gold target and a corridor. Every bucket then rebalances independently whenever it drifts outside its band, and you see every event across the whole retirement.

-

10

De-risk on a glide into retirement

Use Build-Up to see where your buckets would land at retirement versus your target while you're still accumulating, and the exact SIP redirection each year that closes the gap — so you de-risk gradually instead of all at once on the last day.

-

11

Revisit it as life changes — are you still on track?

A retirement plan isn't set once. Come back after a market move, a salary jump, a new goal or each year, update the numbers, and re-run the Verdict and Monte Carlo. Catching a plan drifting off course early is the whole point of having one.

Screens captured from the live app with a demo plan. Figures are illustrative — InvestApps is not a SEBI-registered investment adviser and nothing here is advice. Investment Tracker tour · Terms · Privacy · Refunds